How CAF is Re-Engineering African Football’s Value

Why moving to a quadrennial cycle and embracing "mobile sovereignty" is the most aggressive commercial bet in the continent's history.

Hi everyone! I’m Carla, and this is Off-Ball Logic, a weekly newsletter about the intersection of sports, marketing, and storytelling.

I write about how narratives create value, how identity shapes teams and players, and how the game is sold, told, and understood.

Subscribe to get it in your inbox:

Welcome back to Off-Ball Logic.

Today’s issue explores one of the most aggressive repositioning strategies in global sport: how CAF is using scarcity and mobile-first distribution to revalue African football.

The continent is seeing its biggest media shake-up since the 90s. The traditional “commercial architecture” of the game is shifting, creating a high-stakes battle between old-school satellite giants and a new wave of mobile-first digital players. Backed by CAF, these aggressive new actors are moving fast to capture the massive growth emerging across the continent.

Scarcity as a Value

In marketing terms, brand equity is often built through the balance of availability and exclusivity.

The primary driver of current market volatility is the radical restructuring of the CAF tournament calendar. For decades, the biennial nature of the Africa Cup of Nations (AFCON) was a point of friction with European clubs. The decision to move to a four-year cycle starting in 2028 marks a watershed moment designed to create commercial scarcity,1 essentially manufacturing FOMO. When a tournament happens every other year, it’s a commodity, when it happens every four years, it’s a “rare event.”

However, this strategic pivot did not come without internal pushback. Many regional leaders feel the move was forced through without the consensus of the whole federation.

“The decision was already made,” said one federation president who did not want to be named. “They said it would be discussed in Morocco, but in the end there was no discussion. We’re killing ourselves. If there had been a general assembly and all the presidents were allowed to vote, it would never have passed.”2

For many Africans, this isn’t only a matter of “watchability.” It is deeply linked to the lost opportunity of seeing a generation’s most iconic players represent their countries on their home continent more frequently. By following the pattern of competitions like the Copa América and the UEFA model, CAF is betting that prestige pricing and exclusivity will outweigh high-frequency exposure.

To fill the financial vacuum in non-AFCON years, CAF is engaging in product diversification with the debut of the African Nations League (ANL) in 2029. The tournament format divides the continent into four geographical zones, with regional qualifiers played during the September and October windows before culminating in a knockout final phase in November.3

The 2025 AFCON edition in Morocco, which concluded just a few weeks ago, is already being framed as the “most successful commercial story in the history of African football,” boasting a 155% increase in corporate partners compared to 2021.4

Here’s an interesting question from Maxwell Kablan: Is change really needed?

He also noted, interestingly, that the tournament secured 23 global sponsors, surpassing the previous record of 17 set during the 2023 edition in Ivory Coast. Worth reading the full breakdown in the link above.

Market Disruption: The New World TV Era

While the tournament structure provides the “what,” the “who” is being reshaped by a fierce battle for market penetration. To understand the current volatility, we have to look at how the traditional dominance of MultiChoice (via SuperSport) and Canal+ has been decisively challenged.

Just before the 2023 AFCON, MultiChoice announced it would not broadcast the tournament, a major blow to its 20 million subscribers.

In late 2023, New World TV (NWTV), a Togolese satellite broadcaster, secured exclusive rights to CAF competitions in 46 sub-Saharan countries, effectively upending the established order.5

The rise of New World TV proves that the big media giants no longer hold all the power. We’ve moved into a "messy" era where rights are split up and sold to the highest bidder.

While this makes African football more valuable, it creates a difficult trade-off: do we focus on maximizing profit or making sure every fan has access to the game?

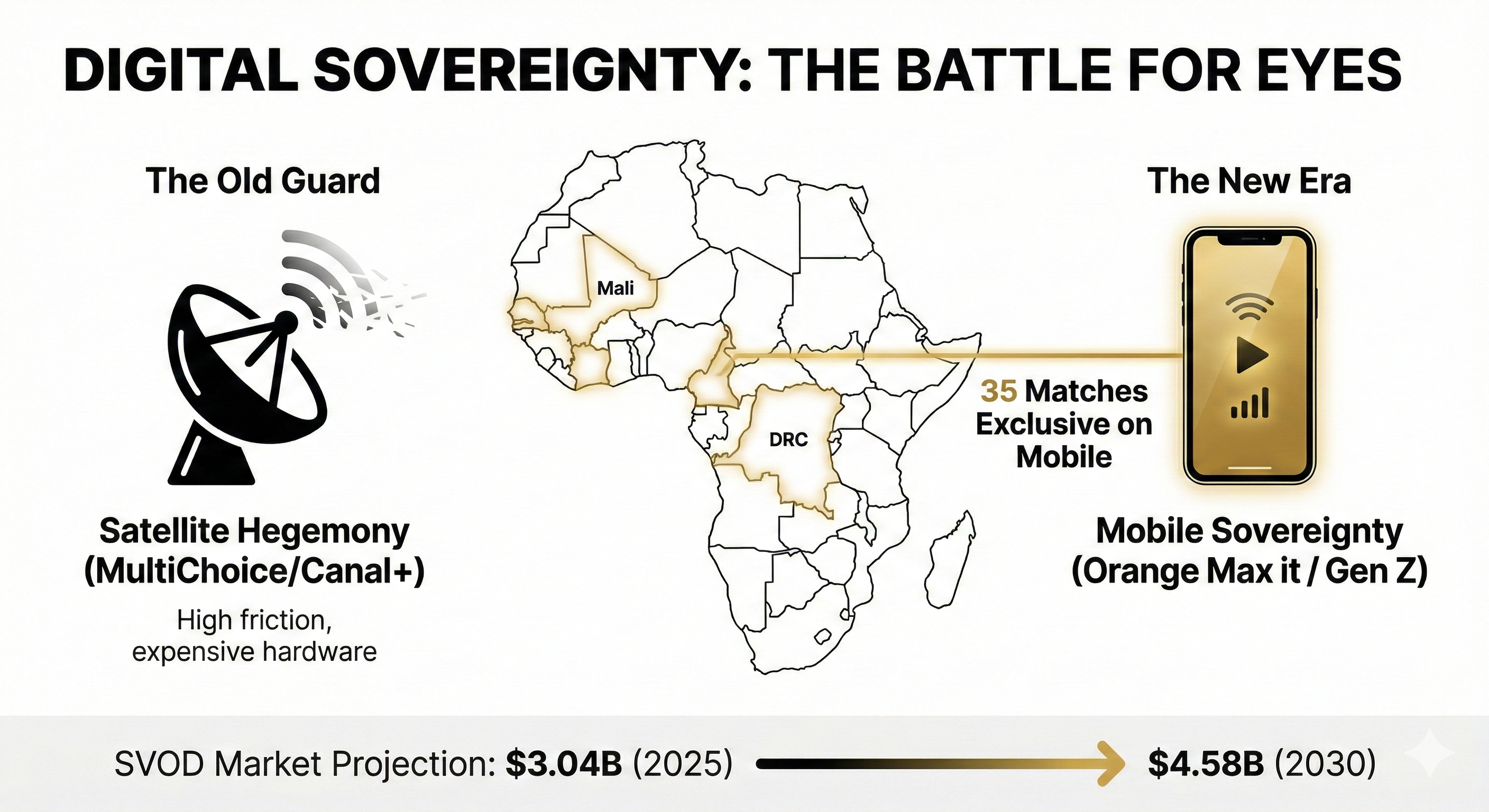

Mobile Screen is the Only Screen

This conflict over broadcast rights isn’t just about which satellite provider wins, it’s about a profound shift in the consumer journey. As fans move away from the traditional television set, the smartphone is becoming the primary stadium for millions. The Africa Subscription Video on Demand (SVOD) market is projected to grow from $3.04 billion in 2025 to $4.58 billion by 2030.6

In a landmark deal, Orange Middle East and Africa (OMEA) secured mobile-only rights for 35 matches via its “Max it” super app. This is a masterclass in increasing Customer Lifetime Value (CLV) by integrating sports content into a broader fintech and communication ecosystem.7

Target Markets: Ivory Coast, Senegal, Cameroon, DRC, Mali.

The Strategy: Integrating live football into a super-app that provides financial and communication services, creating a digital ecosystem that bypasses satellite entirely.

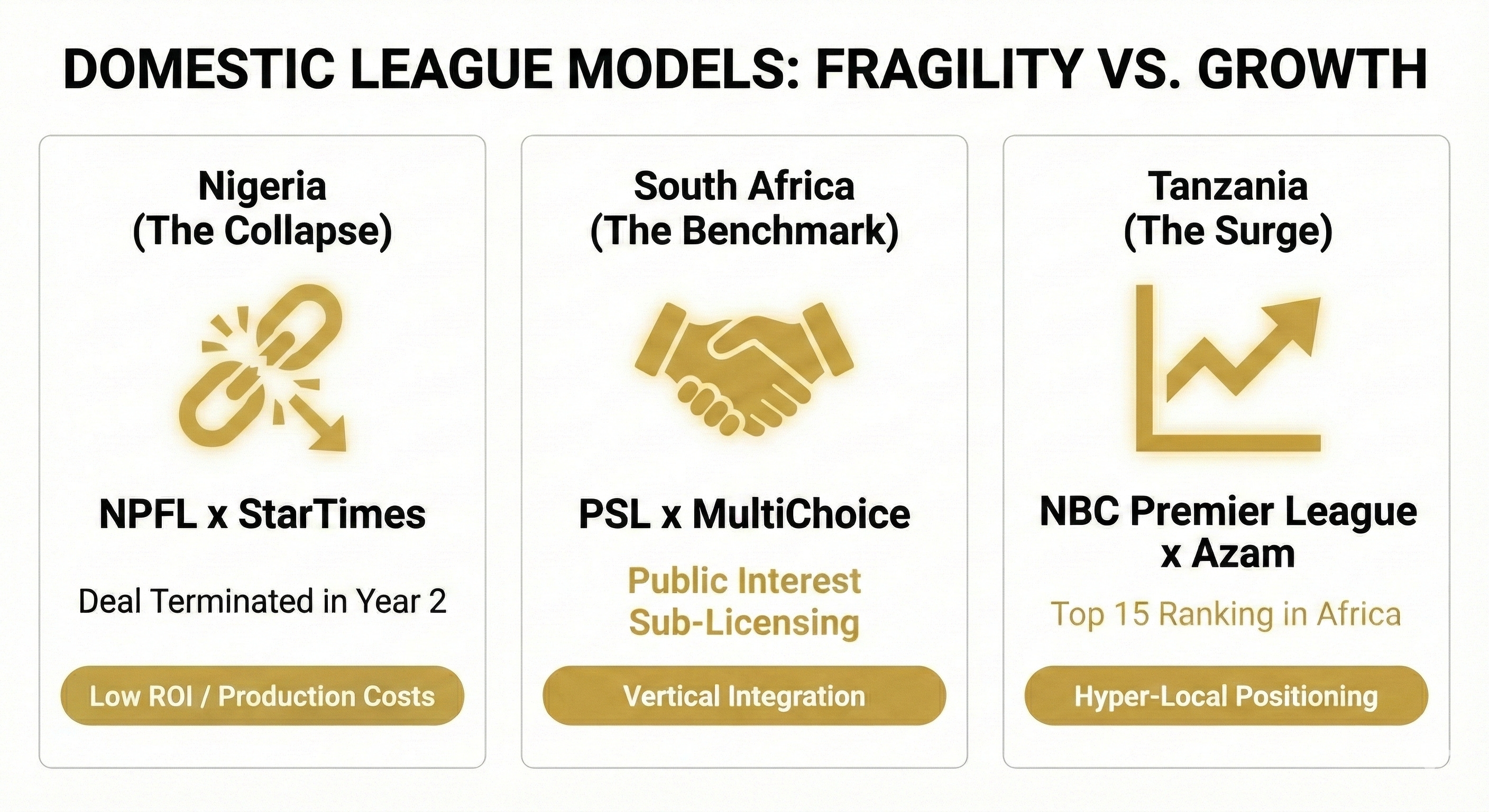

A Tale of Two Models

The success of these continental, digital-first experiments highlights a stark dichotomy when we look at domestic leagues. While CAF-level properties are thriving under this new digital sovereignty, domestic products show a mix of economic fragility and localized growth.

The Nigerian Collapse (Low ROI): In August 2025, the five-year, 6 billion Nigerian naira (approx. 4 million USD) deal between the NPFL and StarTimes terminated after only two years. The failure was attributed to low decoder sales (poor market fit) and skyrocketing production costs.8

The South African Benchmark (Vertical Integration): The PSL continues to set the standard, utilizing a “dominant firm” principle where MultiChoice secures exclusive rights and sub-licenses “public interest” matches. This maintains high brand equity for the primary broadcaster while ensuring broad visibility.9

The Tanzanian Surge (Hyper-local Positioning): Driven by Azam TV, the NBC Premier League has become a reliable economic engine, successfully positioning itself as the premier sports brand in East Africa.10

The “Big Money” Debate

The disconnect between thriving continental events and struggling domestic leagues comes down to one marketing reality: fragmentation is a bad product.

Big brands and investors look for a “clean buy”: centralized rights, consistent quality, and easy scale. Most domestic leagues are currently “unpackaged” products, operating in market-by-market silos that are too messy for global sponsors to touch. Without a centralized story to sell, there’s no way to build real brand equity.

As a result, the money is pivoting toward narrative equity. Elite players have become portable media brands that are easier to buy into than the leagues themselves. Until domestic systems fix their “product packaging” and centralize their rights, the big checks will stay concentrated at the poles: the global superstars and the continental giants.

Conclusion

The shift from satellite to mobile is inevitable, but the transition will be messy. While the “scarcity model” looks great on a pitch deck, the reality of the Nigerian league’s deal collapse proves that product-market fit is still the ultimate judge.

We are entering a period of volatility. The winners won’t necessarily be the ones with the best players, but the ones who can reduce the friction between the fan and the screen. Africa is no longer just a talent export hub but rather is becoming a media innovation lab, and the rest of the football world should be taking notes.

Next Week: We are shifting gears to look at the “Messi Effect.” We’ll analyze the hard numbers behind the hype in: How Inter Miami and MLS revenue changed after Messi.

Carla | Off-Ball Logic

This was a great read, you can really tell how much research and thought went into it. The push and pull you describe between building relevance at the continental (or confederation) level while not leaving domestic leagues behind, really comes through. From a U.S. perspective, this was actually the first AFCON where I noticed a more intentional effort around promotion and highlights, which felt like progress. That said, the matches were still difficult to access here unless you already had beIN, so there’s clearly more room to grow on the distribution side. Lastly, I hope there is a way the domestic leagues in Africa can get stronger from this, which in turn will help the African player.

Good signals here. Your marketing expertise is apparent. Valuable in this sports ecosystem right now.